In a perfect world every Association would have an adequate level of reserves to cover the cost of future capital replacement projects. This requires Associations to have an understanding of their community’s long-term financial needs. But it is not a perfect world. Many Associations end up short on reserves due to a lack of long-term planning, unforeseen replacement projects, or a greater than anticipated scope and/or cost of a particular replacement project. Without sufficient reserves, Boards are faced with two decisions; 1. Increase cash-flow to cover the cost of a particular project or, 2. Defer a replacement, which may result in higher costs or additional repairs.

If communities want to avoid project deferrals, there are several means for an Association to increase cash- flow to cover such costs.

- Reserve Contributions – This is the ideal option as reserves can be established and built-up over time. This option allows homeowners to plan ahead and be financially prepared.

- Special Assessments – This option is the most burdensome to homeowners, boards and managers. This option usually puts significant financial pressure on residents.

- Bank Loans – This option provides an Association with immediate cash-flow to cover an expense. Homeowners are not asked for immediate contributions. However, this option has the added expense of loan interest associated with it.

- A combination of any of the above options.

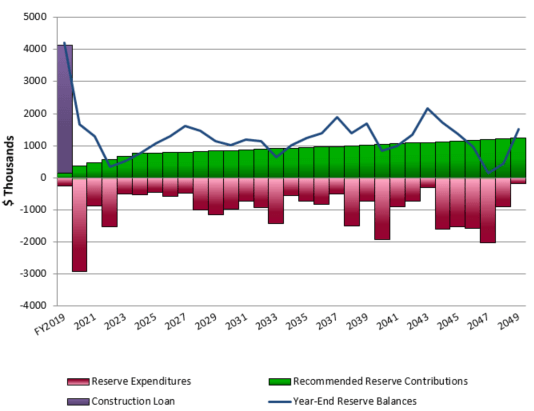

When facing a structural or life-safety related expense, Associations with a shortfall in reserves may have to special assess and/or take out a bank loan. Associations facing such situations can incorporate a financing option within a reserve study to fund major replacements. This option is a long-range financial plan that uses a combination of reserve contributions and a loan to finance specific capital expenditures. The purpose of this option is to avoid special assessments and to minimize the increase in dues posed by repayment of a loan.

A reserve study with the financing option will define the scope of current and future replacement projects and determine whether or not you have sufficient reserves. It will answer if you are likely to exhaust reserves on a replacement project and the merits of doing a special assessment versus financing all or a portion of the project. Having this information available is key for Boards to decide whether to borrow.

An application for a loan is required and lenders want assurance that it will be paid back. Associations will be required to supply financial statements and disclose the amount of existing reserves and the need for future reserves. They will also have to prove whether or not they are budgeting reserve contributions to fund replacements outside the scope of the project financed by the loan. A reserve study with a financing option answers these questions, making the path to secure a loan as efficient as possible.

Most reserve studies include a cash flow analysis, but the reserve study with a financing option goes one step further. It computes the amount of minimal but sufficient reserve contributions necessary over the term of the loan. As loan payments end, greater reserve contributions resume to fund future, less urgent replacements. Changes in the annual budgets are minimized during and after the loan.

The concept is simple, the application a bit complex, but the reward of increased financial security while not burdening homeowners beyond their financial limits is worthwhile. Loan payments, in effect, take the place of some, but not all of the reserve contributions. A reserve study with a financing option gives the Board the facts it needs to make an informed business decision on how to fund a replacement project.